Do International Equities Provide Diversification Benefits?

Over the last decade, U.S. equities have outperformed equities from other countries around the world, and globalization has increased correlations between U.S. and non-U.S. stocks. Many investors, including professional money managers and advisors, have been questioning whether this increased correlation has eliminated the benefits of diversification between U.S. and non-U.S. Equities. To answer that question, I believe that it is important to not just consider the correlation of returns, but also the dispersion of returns.

Over the last decade, U.S. equities have outperformed equities from other countries around the world, and globalization has increased correlations between U.S. and non-U.S. stocks. Many investors, including professional money managers and advisors, have been questioning whether this increased correlation has eliminated the benefits of diversification between U.S. and non-U.S. Equities. To answer that question, I believe that it is important to not just consider the correlation of returns, but also the dispersion of returns.

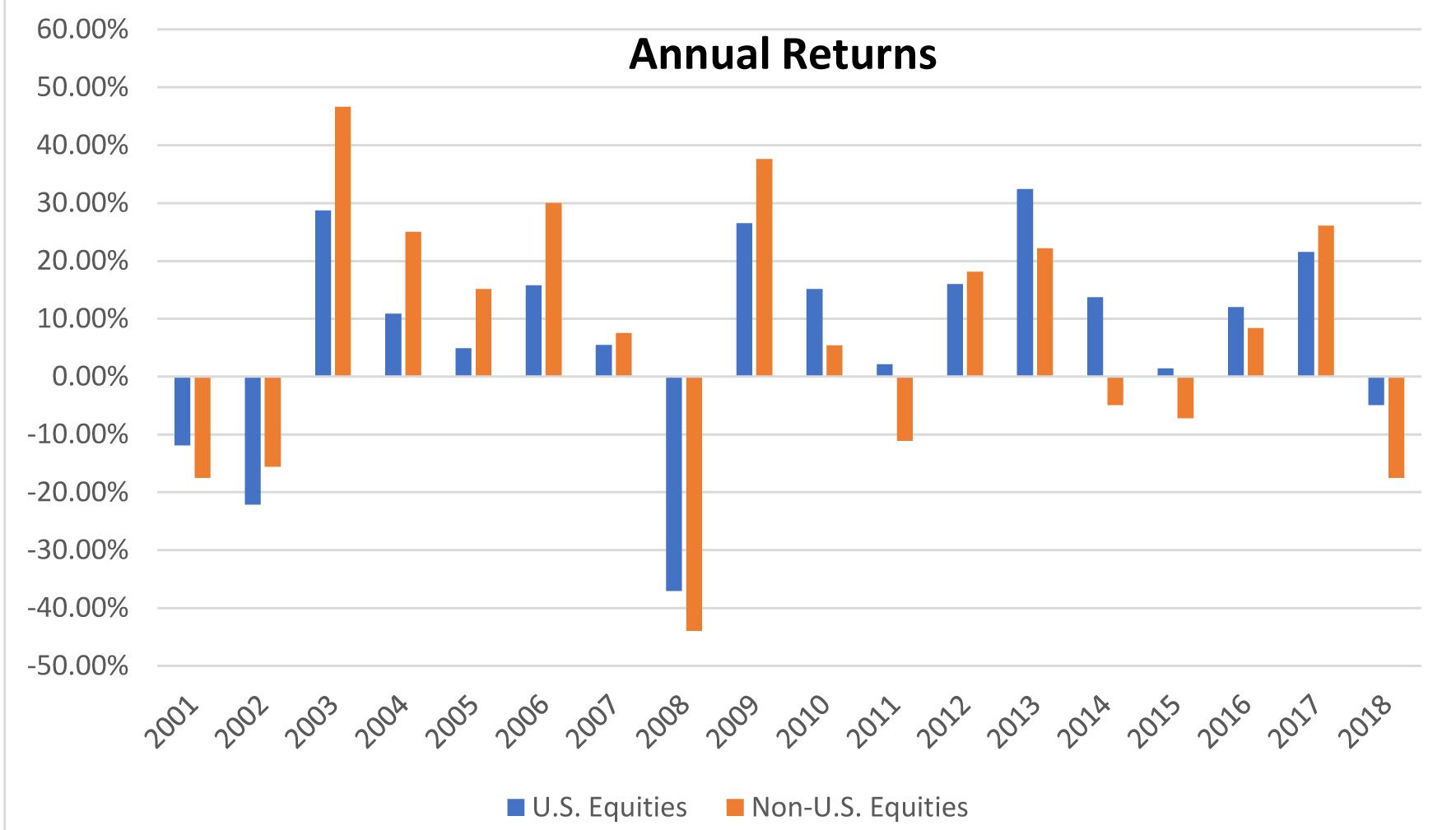

Figure 1 below shows the annual returns for U.S. stocks and non-U.S. stocks from 1/1/2001 through 12/31/2018.

Figure 1

U.S. equities represented by S&P 500; Non-U.S. equities represented by DFA International Value Fund

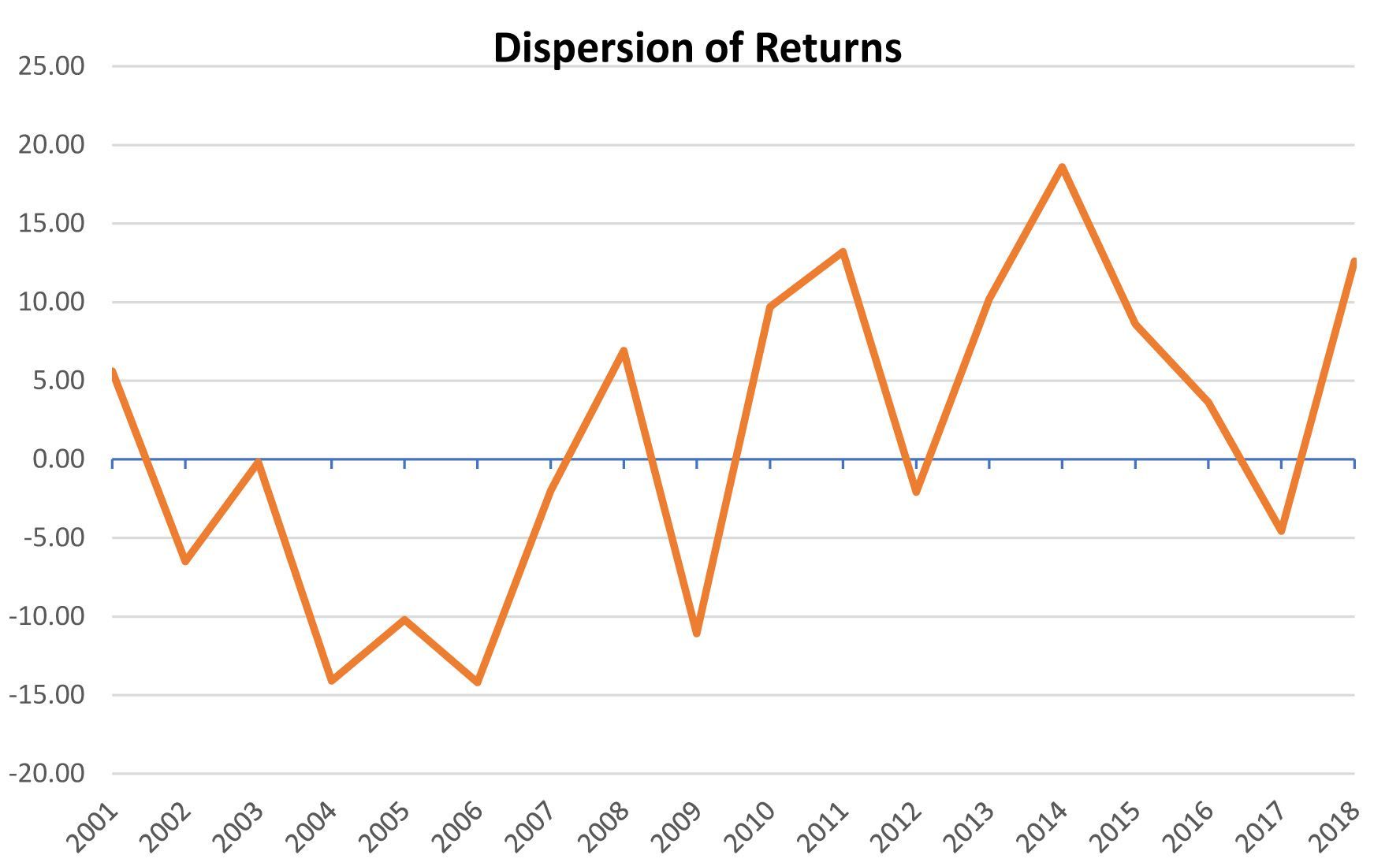

While there were 3 years during this time period where U.S. stocks had a positive return and non-U.S. stocks had a negative return, most of the time, both asset classes moved in the same direction. While the correlations were somewhat high and both asset classes tended to move together, the dispersion of annual returns was also somewhat large. Figure 2 shows the difference between the annual returns of U.S. stocks and non-U.S. stocks (the dispersion of annual returns). Points above the center horizontal line (marked 0.00) show that U.S. stocks outperformed non-U.S. stocks that year and by how much. Points below the 0.00 line show that U.S. stocks underperformed non-U.S. stocks that year and by how much. For example, in 2004, U.S. stocks underperformed non-U.S. stocks by 14.10%.

Figure 2

U.S. equities represented by S&P 500; Non-U.S. equities represented by DFA International Value Fund

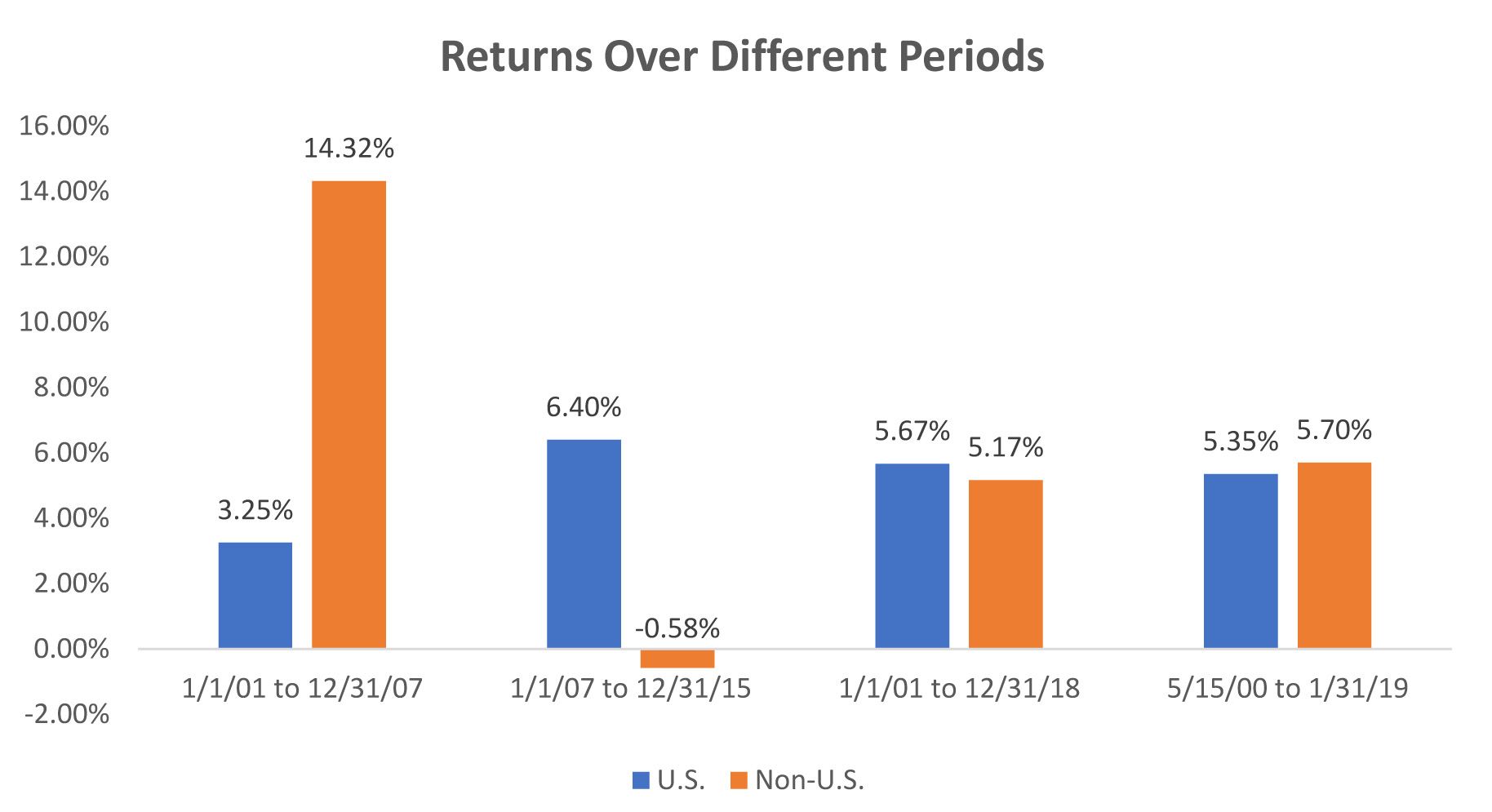

Figure 3 illustrates that while the longer term returns for these two asset classes were similar, each asset class had long periods of outperformance.

Figure 3

U.S. equities represented by S&P 500; Non-U.S. equities represented by DFA International Value Fund

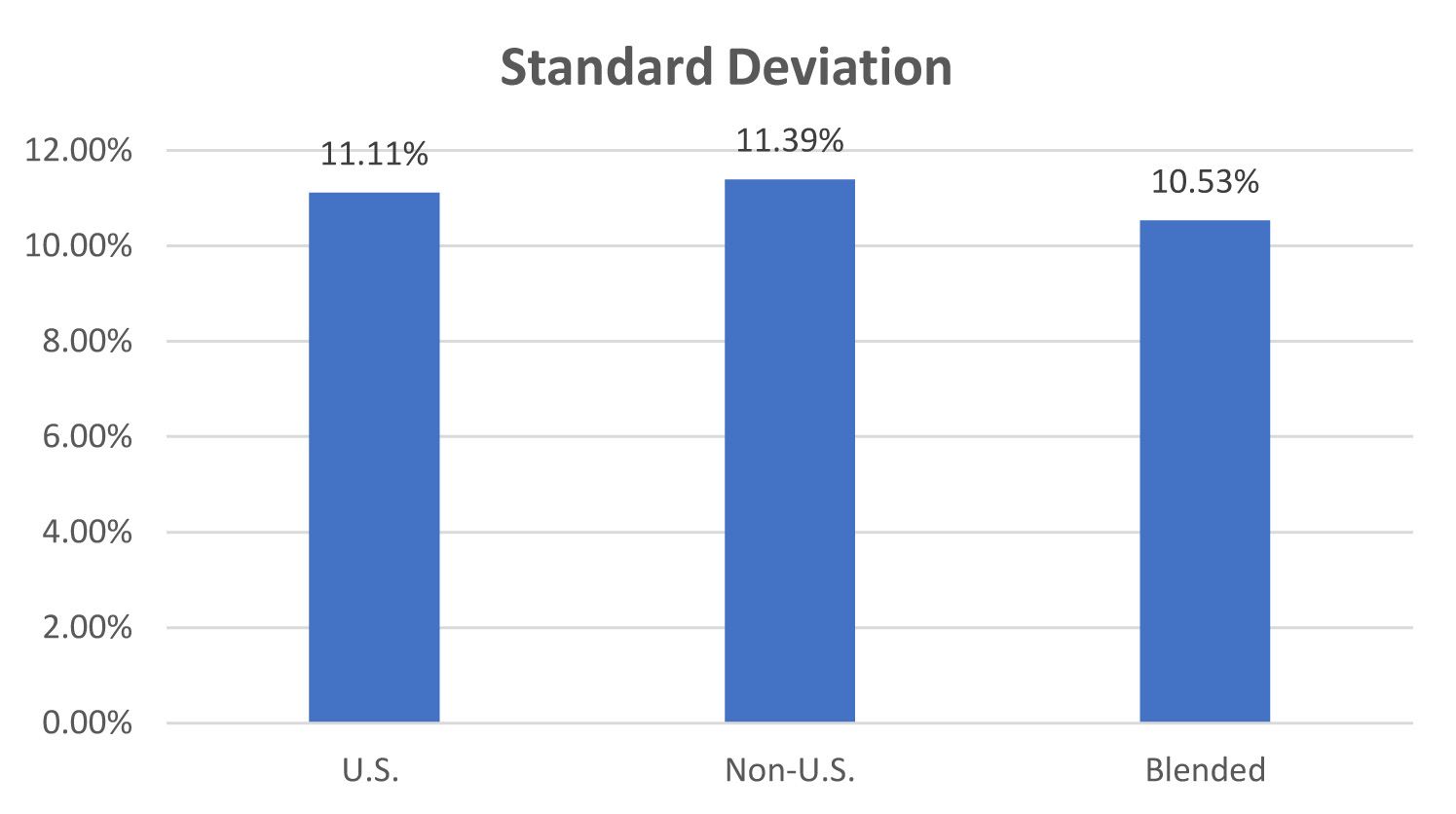

Finally, figure 4 shows the 3-year standard deviation of U.S. equities and non-U.S. equities as well as the standard deviation of a blended portfolio of 60% U.S. equities and 40% non-U.S. equities.

Figure 4

U.S. equities represented by S&P 500; Non-U.S. equities represented by Schwab Fundamental International Developed Large Company Index

With a correlation of .71 over the same 3-year period (ending 1/31/19), these assets didn’t move in exactly the same way, and the portfolio of both U.S. and non-U.S. stocks had slightly lower volatility than either asset on its own.

Conclusion:

The long-term historical returns and long-term expected returns for U.S. equities and non-U.S. equities are very similar. The annual dispersion of returns, however, can be large, and as figure 2 and figure 3 illustrate, there are sometimes long periods of time where U.S. stocks outperform non-U.S. stocks and long periods where they underperform. Owning both U.S. and non-U.S. equities can increase your chances of receiving the long-term expected return with less volatility over time.

Additionally, because these asset classes are not perfectly correlated and don’t move in exactly the same way, a diversification benefit may be realized, especially over longer periods of time that include periods of outperformance and underperformance for U.S. stocks. This diversification benefit can be in the form of increased returns, reduced risk, or both.

When you subscribe to the blog, we will send you an e-mail when there are new updates on the site so you wouldn't miss them.